Introduction: The Wake-Up Call for Cyber Insurance

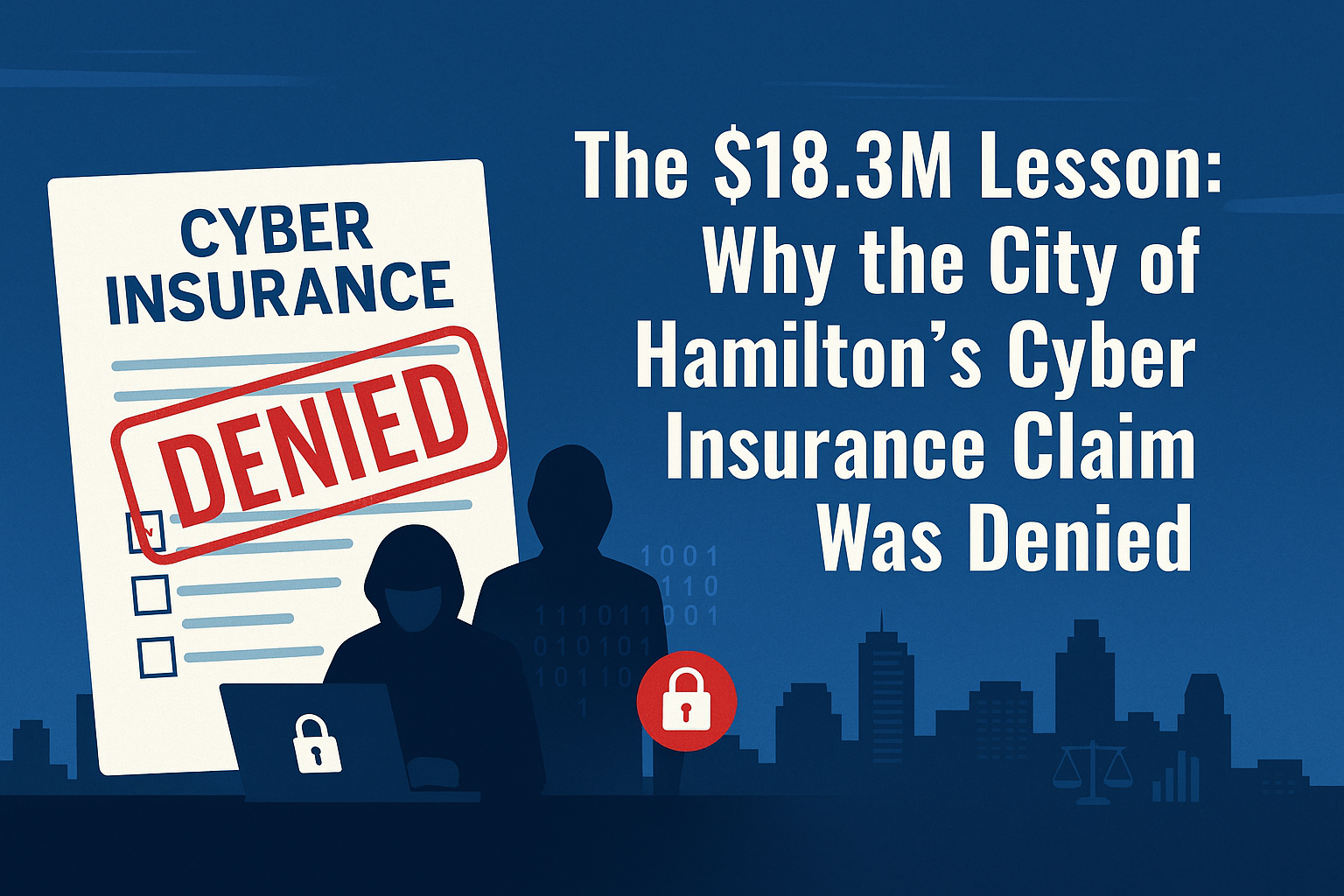

When the City of Hamilton, Ontario, was struck by ransomware in February 2024, officials expected their cyber insurance would cover the recovery bill. Instead, their claim was denied, leaving taxpayers responsible for more than $18.3 million in costs.

The denial was not about the size of the claim or whether insurance applied to ransomware. It came down to one thing: Hamilton had not fully implemented multi-factor authentication (MFA), a requirement of its policy.

For professional services firms like law practices and CPA firms, the lesson is clear. Cyber insurance is not a guarantee. Coverage depends on strict compliance with policy requirements, and failure to meet them can result in devastating financial and reputational losses.

The City of Hamilton Incident

On February 25, 2024, a ransomware attack crippled roughly 80 percent of the City of Hamilton’s municipal systems, including property tax billing, licensing, and transit planning. The attackers demanded a ransom of nearly 18.5 million Canadian dollars. The city refused to pay and chose to rebuild its systems instead.

When Hamilton filed a claim with its cyber insurance provider, the insurer reviewed the details and found the city had not implemented multi-factor authentication across all of its systems. Because this control was required under the terms of the policy, the claim was denied. A third-party review confirmed the decision.

The result was a financial loss of more than 18.3 million dollars, borne entirely by taxpayers.

Why Compliance Matters for Professional Services Firms

Not a Silver Bullet

Cyber insurance is a contract, not a blanket guarantee. Every policy contains specific clauses, exclusions, and conditions. Coverage only applies if those conditions are met.

Due Care vs. Good Faith

Insurers require demonstrable proof of due care. Deploying multi-factor authentication, testing backups, and enforcing email security are not optional. If your firm cannot prove compliance, the insurer can and will deny a claim.

The Financial and Reputational Risk

A ransomware breach is damaging enough on its own. A denied insurance claim can be catastrophic. The City of Hamilton’s case is now a cautionary precedent.

Adding to this risk, modern ransomware groups increasingly use extortion tactics rather than encryption alone. They steal sensitive information and threaten to publish it if payment is not made. For law firms, this could expose privileged communications and case files. For accounting firms, it could mean client financial records, payroll data, or tax IDs posted online.

Even if your firm has secure backups and can restore operations quickly, the reputational fallout from leaked client information can permanently erode trust. Unlike technical downtime, reputational damage cannot be undone by insurance or technology.

What Law and Accounting Firms Must Do

This is not just a cautionary tale. It is a practical roadmap for action.

Step 1: Read and Understand the Policy Fine Print

Identify every security requirement. Do not assume coverage extends automatically to all incidents.

Step 2: Do Not Assume You Are Covered

Confirm, through testing and documentation, that your firm meets the stated requirements. This includes MFA, secure backups, and a documented incident response plan.

Step 3: Implement the Non-Negotiables

- Multi-Factor Authentication (MFA): The critical missing link in Hamilton’s case.

- Regular, tested, and offline backups: Insurers expect resilient recovery strategies. But backups alone are no longer sufficient in the age of double and triple extortion ransomware.

- Email security and anti-phishing training: Professional service firms are constant phishing targets during tax season, litigation, and high-value transactions.

- Endpoint Detection and Response (EDR): Many insurers now require it as a replacement for traditional antivirus.

Step 4: Engage a Cyber-Savvy Managed Service Provider

Professional services firms often lack the internal resources to meet these requirements. An experienced MSP can:

- Implement the controls insurers require

- Provide documentation, logs, and compliance evidence

- Serve as a credible partner during claim investigations

Conclusion: Cyber Insurance Is Only as Strong as Your Baseline Controls

Cyber insurance is indispensable, but it only works if you meet the conditions of coverage. Hamilton’s experience demonstrates that even well-resourced organizations can be denied claims when controls are incomplete.

For law firms and accounting firms, the stakes are even higher. Beyond the financial loss, a denial can expose your firm to regulatory investigations, professional discipline, and permanent damage to client trust.

Hamilton’s story is a public example of a private nightmare that could happen to any firm. By reviewing your policy, validating compliance, and addressing gaps now, you can ensure that your cyber insurance will protect you when you need it most.

Contact us to schedule a Cyber Insurance Readiness Assessment designed specifically for law and accounting firms. Ensure that your controls align with policy requirements and that your firm is protected both financially and professionally.